On June 14, 2026, the United States and Iran finalized an interim peace agreement mediated by Pakistan, ending a volatile four-month regional conflict. While the primary relief is geopolitical, the economic ripple effects will fundamentally alter global supply chains, energy markets, and monetary policy trajectories.

For macroeconomic analysts, this accord represents a massive supply-side shock. Here is a breakdown of every core economic and structural catalyst outlined in the deal and their anticipated impact on global markets.

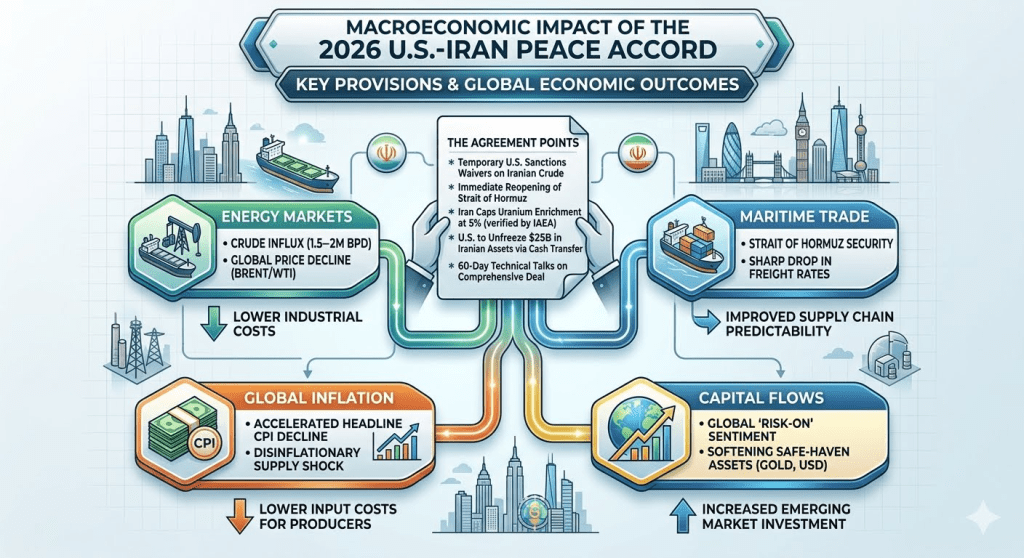

1. Complete Breakdown of the Accord’s Terms

The interim agreement, which serves as a binding memorandum of understanding, contains six non-negotiable pillars that take immediate effect ahead of the formal signing ceremony in Switzerland on Friday, June 19, 2026:

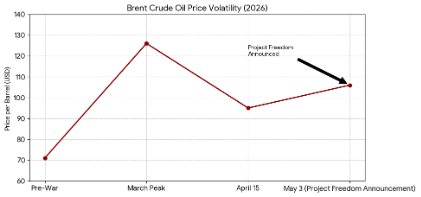

- Immediate Ceasefire: Permanent termination of military operations on all fronts, including conflicts involving Hezbollah in Lebanon, stripping the structural “war premium” out of global commodity markets.

- Reopening the Strait of Hormuz: Iran must immediately open the maritime corridor to all commercial vessels, eliminating severe logistics bottlenecks.

- Lifting the Naval Blockade: U.S. President Donald Trump authorized the complete removal of the U.S. naval blockade on Iran, restoring normal shipping lane capacity.

- Oil Sanctions Waivers: The U.S. will temporarily waive oil sanctions, legally allowing Iran to inject 1.5 to 2 million barrels per day (bpd) back into the global supply.

- $25 Billion Cash Transfer: The U.S. will release $25 billion in frozen Iranian assets via direct cash transfers, drastically shifting regional liquidity.

- Nuclear Freeze & Stockpile Negotiation: Iran must immediately pause uranium enrichment and facility expansion. A strict 60-day window of technical talks begins now to negotiate the permanent destruction or dilution of its highly enriched uranium stockpile.

2. Market Impact Analysis

Energy Sector: A Sudden Supply Influx

The immediate legal flow of Iranian crude will heavily disrupt a tightly balanced global energy market. Expect rapid downward pressure on Brent and WTI crude futures. A sustained oil price drop acts as an organic, cross-border tax cut for importing nations, boosting consumer disposable income and lowering industrial input costs.

Supply Chains: Reopening the Global Chokepoint

The Strait of Hormuz handles roughly 20% of the world’s petroleum. Opening it instantly eliminates hyper-inflated war-risk insurance premiums for maritime shipping. Freight rates for tankers and container ships in the Middle East will plummet, alleviating lingering global transit inflation and restoring predictability to European and Asian supply chains.

Inflation and Central Bank Trajectories

Prior to the accord, central banks were bracing for stagflationary pressures driven by energy spikes. This disinflationary impulse will accelerate the decline of headline Consumer Price Index (CPI) metrics globally. Lower structural inflation gives the Federal Reserve and the European Central Bank (ECB) room to halt rate hikes or pivot toward monetary easing, supporting global GDP growth.

Capital Flows and Asset Reallocation

The $25 billion liquidity injection combined with geopolitical de-escalation will trigger a strong “risk-on” environment. Capital is expected to exit traditional safe havens like Gold and the U.S. Dollar, rotating back into emerging markets and global equities.

The Bottom Line

The 2026 U.S.-Iran Peace Accord is a net-positive supply shock for the global economy. By lowering energy costs, restoring vital trade corridors, and mitigating geopolitical risk premiums, the agreement provides a stabilizing anchor for global growth. However, long-term market stability hinges entirely on compliance during the next 60 days of technical nuclear talks.

Market analysis provided by The Macro Compass is for informational purposes only. Please consult with a financial advisor before making investment decisions.