Today delivered a one-two punch for markets: a closely watched Producer Price Index (PPI) report in the morning, followed by the Federal Reserve’s FOMC decision in the afternoon.

The result? A volatile session that reflected a market struggling to reconcile persistent inflation with a cautious central bank.

📊 Morning Shock: PPI Reinforces Inflation Concerns

The day started with the release of the latest PPI data at 8:30 AM ET—a key measure of wholesale inflation.

Recent trends have shown PPI coming in hotter than expected, with prior readings around +0.5% month-over-month vs. +0.3% expected, and core components even stronger. (XTB Broker Online)

That matters because PPI often feeds into future consumer inflation (CPI).

Today’s takeaway:

- Inflation pressures—especially in services—remain sticky

- The idea of quick rate cuts is fading

- Markets immediately leaned risk-off

Historically, strong PPI prints tend to push equities lower because they signal the Fed may need to keep rates higher for longer.

🏛️ Afternoon: Fed Holds Rates, But Tone Matters

Later in the day, the Federal Open Market Committee (FOMC) announced its rate decision.

As expected, the Fed held rates steady in the 3.50%–3.75% range. (Wikipedia)

But the decision itself wasn’t the story—the messaging was.

Markets were focused on:

- Future rate cut timing

- Inflation outlook

- Economic projections

Coming into the meeting, expectations were already shifting toward fewer or later rate cuts, especially after recent inflation data. (GO Markets)

📉 Market Reaction: A Tug-of-War Between Inflation and Policy

The market reaction today can be summed up in one word: conflicted.

After PPI:

- Stocks moved lower

- Yields and inflation fears rose

- Rate-cut expectations were pushed further out

After FOMC:

- Initial reaction depended on interpretation of Fed tone

- Markets attempted to stabilize, but conviction remained low

This creates a classic push-pull dynamic:

- Inflation data → bearish (higher rates longer)

- Fed pause → mildly supportive (no immediate tightening)

⚡ The Bigger Picture: Why Today Matters

Today wasn’t just about one data point or one Fed meeting—it highlighted a broader market theme:

👉 The last mile of inflation is proving difficult.

- Goods inflation is easing

- Services inflation remains sticky

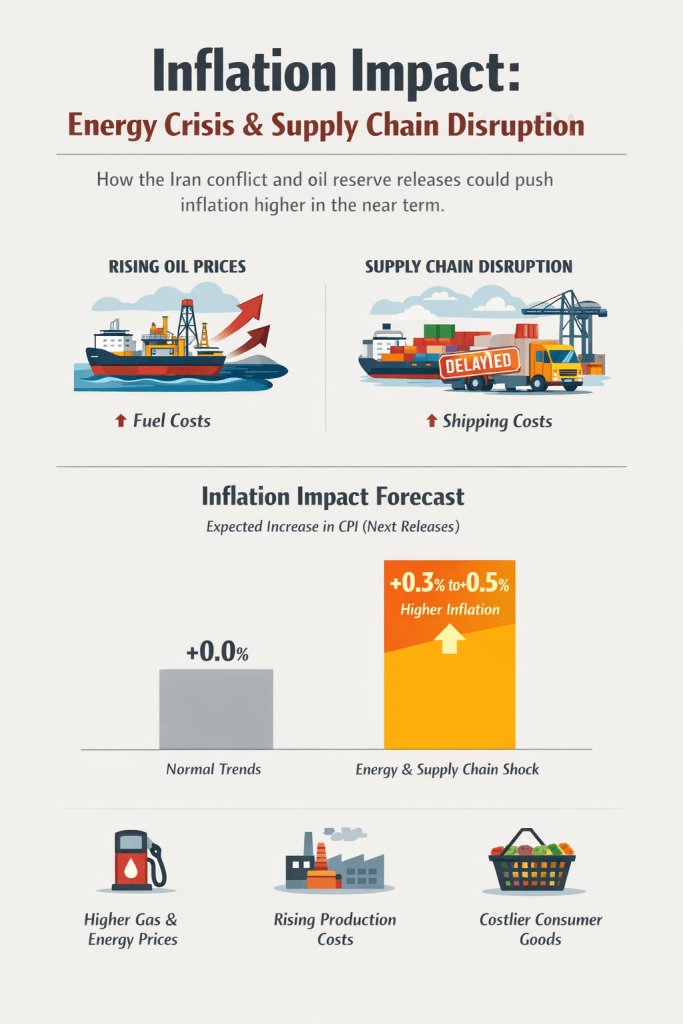

- Energy prices (partly due to geopolitical tensions) add uncertainty

This combination makes the Fed’s job harder and keeps markets on edge.

🔮 What Comes Next

Markets are now recalibrating around a few key questions:

- Will inflation stay elevated longer than expected?

- Are rate cuts being pushed into the second half of the year?

- Can the economy handle higher rates without slowing sharply?

Expect:

- Continued volatility around economic data releases

- Increased sensitivity to inflation prints

- More choppy, headline-driven trading

✅ Bottom Line

Today’s market action reflects a simple but powerful reality:

- Inflation is not fully under control

- The Fed is in wait-and-see mode

- Markets are adjusting to “higher for longer”

Until there is clearer evidence that inflation is cooling, expect markets to remain reactive, volatile, and highly data-dependent.